In 2019, strategic-beta exchange-traded products in the Asia-Pacific region recorded another year of strong growth in collective assets under management, with assets in strategic-beta ETPs growing 43% to USD 34.5 billion, Morningstar’s latest research funds. The growth was driven by a combination of double-digit market gains and net flows into new and existing products.

In Morningstar’s latest research titled A Global Guide to Strategic-Beta Exchange-Traded Products, authored by Morningstar researchers Alex Bryan, Jackie Choy, Kongkon Gogoi, Ben Johnson, and Kenneth Lamont, the authors find that through over the past decade-plus, the strategic-beta space has grown more rapidly than the broader exchange-traded product market, new product launches have dwindled, and fees have come under pressure. “Strategic-beta ETPs’ growth has been driven by new cash flows, new launches, and the entrance of new players. However, more recently, these products’ market-share gains have stalled. This market segment is showing signs of maturity,” the report finds. You can get a copy of the report here.

Strategic Beta in a Time of the Coronavirus

The authors acknowledge that the COVID-19 crisis has roiled markets.

“This episode reinforced important lessons about strategic-beta approaches to portfolio construction and taught some new ones about how these products perform in stressed markets,” the authors note.

Strategic beta is an active approach to portfolio construction. Strategic-beta ETPs’ performance through recent market volatility underscores the fact that—like discretionary active portfolios—no two of these products are created equal.

“Our analysis of their performance during the first five months of 2020 reveals the differences between them and emphasizes the importance of thorough due diligence when selecting from the strategic-beta ETP menu,” the report notes.

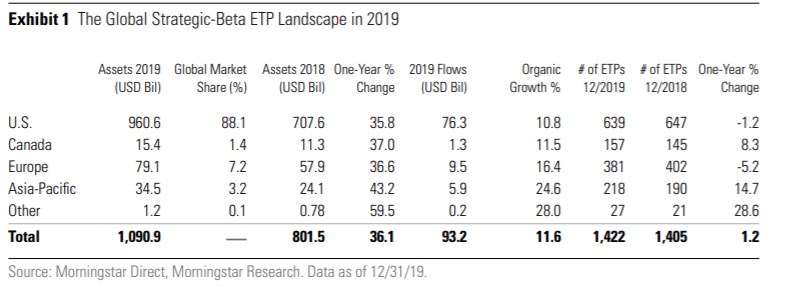

Global Strategic Beta

As of Dec. 31, 2019, there were 1,422 strategic-beta ETPs worldwide, with collective assets under management of approximately $1.09 trillion. Assets in these products grew 36.1% in 2019. Top-line growth was buoyed by rallying equity markets, as the Morningstar Global Markets Index gained nearly 27%. Strategic-beta ETPs amassed $93.2 billion in net new cash flows, translating into organic growth of 11.6%, the report notes, adding that the slowing pace of new product launches and intensifying fee competition are signs that the space is maturing. The number of strategic-beta ETPs increased just 1.2% in 2019.

In the United States, the number of new product launches was the lowest since 2010 and, for the first time ever, was eclipsed by the number of strategic-beta ETPs that were shuttered. This is clear evidence that the menu has been oversaturated. A crowded and competitive landscape will continue to put downward pressure on fees. Low-volatility ETPs continued to gain market share in the U.S., Europe, and Canada in 2019.

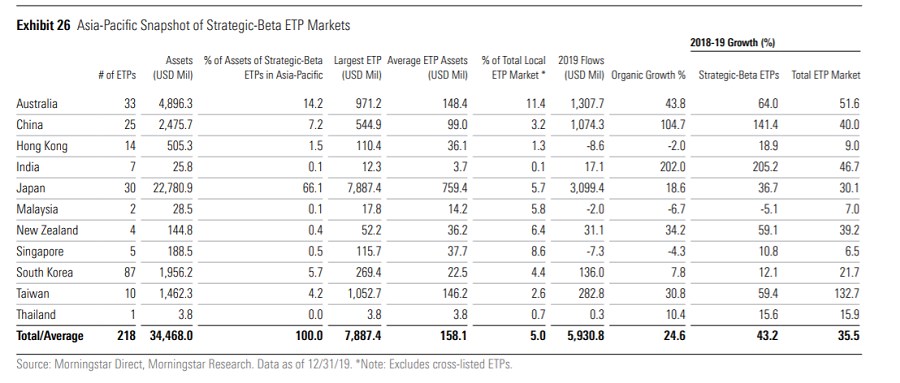

Eye on APAC

The report finds that many markets within the Asia-Pacific region recorded growth in strategic-beta ETP assets in excess of 50%. These include Australia, China, India, New Zealand, and Taiwan. The number of strategic-beta ETPs grew to 218 from 190 a year earlier. Most new launches came from China and South Korea. The Asia-Pacific strategic-beta ETP league table didn’t change much in 2019, aside from the fact that assets ballooned. The region’s strategic-beta ETP market remained fragmented. Beyond the 10 largest ETP providers, there were a total of 168 ETPs managed by 53 different ETP providers occupying a collective market share of only 19%.

From a country perspective, the Bank of Japan’s ongoing ETF purchases served to cement Japan’s leading position, with $22.8 billion in strategic-beta ETP assets as of the end of 2019. Australia was a distant second with $4.9 billion in assets. China overtook South Korea to finish 2019 in third place with $2.5 billion invested in strategic-beta ETPs. China’s strategic-beta ETP lineup almost doubled in number and more than doubled in assets.

Strategic-beta ETPs’ penetration varies widely across the region. Market shares range from 0.1% to 11.4%. Australia has seen the greatest adoption, where strategic-beta ETPs account for 11.4% of local ETP assets. Singapore has the next-highest level of strategic-beta ETP market share in the region at 8.6%.

Exchange-traded products belonging to the Quality strategic-beta group retained the top position in the asset rankings in 2019. These ETPs had a 62% share of the Asia-Pacific strategic-beta ETP market. The 31 ETPs that belong to this group hold $21.5 billion, up 49% from a year earlier.

Who Should Buy Strategic-Beta Products?

As always, investors should invest based on their own personal situation. Before investing, investors should also understand their financial goals, time horizons, and risk appetites. Having said that, strategic-beta ETPs might make sense for some investors.

“Investors who are looking for active exposure to a specific style (for example, value, growth, momentum, or low volatility) might consider strategic-beta funds as an alternative to a fully active manager. Their lower costs and propensity to stay true to a stated style make them advantageous for investors who seek these traits,” points out Ian Tam, Morningstar Canada’s director of investment research. He adds that conservative investors might consider low- or minimum-volatility strategic-beta products if they are seeking a less bumpy ride than a broad market index.

He adds that strategic-beta funds typically leverage a set of quantitative screening criteria to come up with investment decisions. “The advantage of this is that the investment process is extremely consistent. As such, it helps if you have an understanding of the fund’s underlying investment strategy, so that the outcomes do not catch you off guard. Investors should know that not all styles will outperform in each market. More aggressive styles like momentum and growth-oriented strategic-beta products are expected to outperform in up markets and underperform in down markets. The opposite can be true for low-volatility strategic-beta products. Investors are remined that these products should stay true to their style, for better or worse,” he warns.

.png)