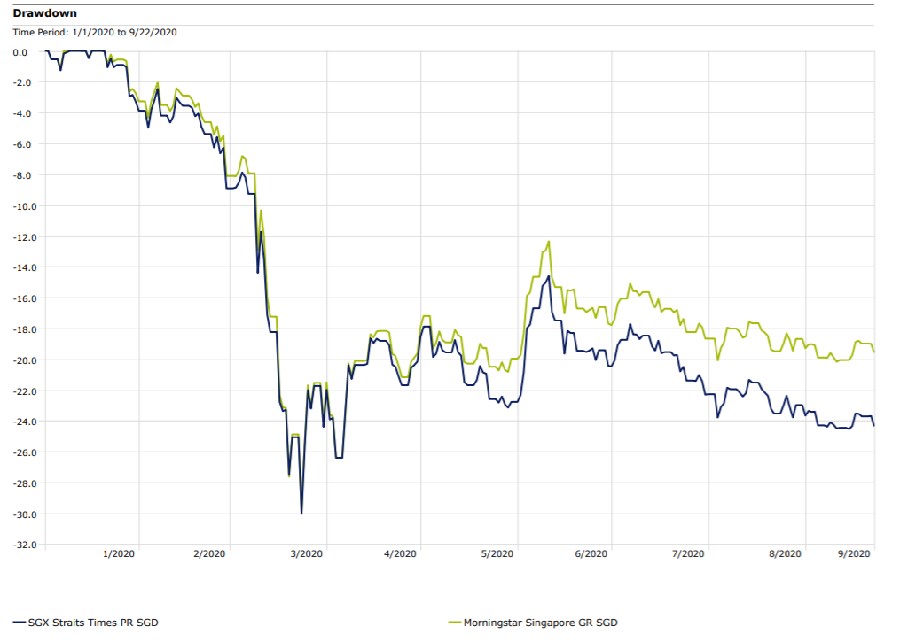

Well, that was quick. Despite the bleak global economic outlook and the continued uncertainty brought on by the coronavirus pandemic, as of the end of August 2020, the stock markets have recovered to pre-pandemic highs.

Morningstar Canada’s director of investment research Ian Tam used the concept of the “pain index” coined by Dr. Paul Kaplan and showed that the COVID-19 bear market goes down in history as one of the least painful on record, lasting a total of about 120 trading days, with a mazimum drawdown of about 30%.

Stars

There are still some stocks in our coverage universe in Singapore that are undervalued. We have presented four here. These stocks all have a Morningstar Star Rating of five stars. The star rating is determined by three factors: a stock's current price, Morningstar's estimate of the stock's fair value, and the uncertainty rating of the fair value. The bigger the discount, the higher the star rating. Four- and 5-star ratings mean the stock is undervalued, while a 3-star rating means it's fairly valued, and 1- and 2-star stocks are overvalued.

Moats

Four of these stocks have a ‘Narrow’ economic moat. The Morningstar Economic Moat Rating represents a company's sustainable competitive advantage. A company with an economic moat can fend off competition and earn high returns on capital for many years to come.

Morningstar has identified five sources of ‘moat’:

-Switching costs are those obstacles that keep customers from changing from one product to another.

-The network effect occurs when the value of a good or service increases for both new and existing users as more people use that good or service.

-Intangible assets are things such as patents, government licenses, and brand identity that keep competitors at bay.

-A company with a cost advantage can produce goods or services at a lower cost, allowing them to undercut their competitors or achieve higher profitability.

-Efficient scale benefits companies operating in a market that only supports one or a few competitors, limiting rivalry.

A company whose competitive advantages we expect to last more than 20 years has a wide moat; one that can fend off their rivals for 10 years has a narrow moat; while a firm with either no advantage or one that we think will quickly dissipate has no moat. All three stocks have a ‘Stable’ moat trend. Finally, it pays to remember that these stocks have high or medium fair value uncertainty.

With these details out of the way, let’s look at the stocks.

| Name | Morningstar Star Rating | Economic Moat | Moat Trend | Fair Value Incertainty |

| Keppel Corp Ltd | 5 | None | Stable | Medium |

| CapitaLand Mall Trust | 5 | Narrow | Stable | Low |

| Hongkong Land Holdings Ltd | 5 | Narrow | Stable | Low |

| CapitaLand Ltd | 5 | Narrow | Stable | Medium |

Morningstar Direct Data as of September 23

Keppel Corp

Being the largest ship and rig builder in Singapore, Keppel effectively operates as a duopoly together with its peer Sembcorp Marine. The company’s nearly two dozen shipyards are strategically located across all major offshore oil-producing regions, near its clients. This gives the firm an unrivalled advantage, as it can repair and upgrade vessels locally in a highly responsive manner and provide locally-based solutions to contract changes and variations from national oil companies.

Morningstar Senior Equity Analyst Chokwai Lee had previously assigned Keppel a narrow moat rating, the sharp fall in oil prices since mid-2014 has challenged his view, with the firm’s return on invested capital, or ROIC, falling below its weighted average cost of capital, or WACC, in 2016. “Even though it still possesses some intangible assets (a skilled workforce and proprietary knowledge in high-specification vessel design) that could normally constitute a moat, we believe Keppel is in the early stages of a multiyear turnaround,” Lee says.

He pegs Keppel’s fair value estimate at SGD 7.00 despite Temasek’s decision to withdraw its partial offer (an additional 30.55% stake at SGD 7.35 per share). “We think this would be negative to near-term sentiment but our valuation on Keppel is not conditional on Temasek’s offer. More importantly, Temasek remains Keppel's largest shareholder with about 20% direct stake. We believe Keppel remains undervalued at the current share price, underpinned by its diversified businesses, which continue to do reasonably well during the COVID-19 outbreak,” Lee says.

CapitaLand Mall Trust

CapitaLand Mall Trust, or CMT, owns a portfolio of high-quality malls and retail properties in Singapore and boasts the greatest market share in retail space. Its malls are well managed, situated in densely populated areas, and close to mass transport hubs with high footfall. These attributes are attractive for its diverse tenant base, resulting in high retention rates and near-full occupancy across its properties through business cycles.

Morningstar analyst Ken Foong believes CapitaLand Mall Trust has a narrow economic moat, derived from efficient scale and the network effect. He assigns the stock a fair value of SGD 2.54 per unit (lowered from SGD 2.56) after fine-tuning his model.

“Uncertainties remain in the near term due to COVID-19 and will continue to result in unit price volatility, in our view. However, we think the units are undervalued at the current price and offer an attractive opportunity for investors willing to look beyond COVID-19,” he says.

Hongkong Land Holdings

As Hong Kong’s second-largest office landlord (behind Swire Properties), but one with the most centrally located assets, Hongkong Land is the clear beneficiary of the recent boom in the region’s office sector. Driven by strong demands from Chinese corporates establishing a presence in the city, office buildings in the CBD are in high demand. Chinese corporates are particularly attracted to the high-grade office spaces offered by Hongkong Land.

Morningstar analyst Phillip Zhong has lowered his fair value estimate to USD 7.55 from USD 8 per share while maintaining the company's narrow moat and stable moat trend ratings. “The overall market environment should bode well for higher completion and booking for the company’s projects as well as higher contract sales for new launches during the second half,” Zhong says.

CapitaLand Commercial Trust

CapitaLand Commercial Trust, or CCT, is a commercial real estate investment trust with properties valued at about SGD 10.5 billion, predominantly located in Singapore’s central business district. Office space in the CBD makes up 48% of the city-state's 57.2 million square feet of total office stock, and CCT's offices make up around a fourth of the 27.6 million square feet in CBD office space.

Foong lowered CapitaLand Commercial Trust’s, or CCT’s, fair value estimate marginally to SGD 2.08 (from SGD 2.10), after taking into account our latest fair value estimate of SGD 2.54 for CapitaLand Mall Trust, or CMT.

“Our base case assumes the merger between CCT and CapitaLand Mall Trust will go through. Our narrow moat and stable moat trend ratings remain unchanged. We believe the coronavirus outbreak will not have huge effects on office REITs. As a proxy to CMT due to the ongoing merger, we think CCT’s units are undervalued at the current price,” he says.

.png)