Last week, we tested a strategy with two Chinese equity indices, and talked about how it timing the market makes you lose out on gains over the long-term. The modeling of index returns concluded that botching a market-timing decision does sacrifice a period of (strong) returns. It proved our point – time in the market is better than timing the market.

Tom Lauricella, Editorial Direct for Professional Audience at Morningstar, explains that ineffective market-timing efforts can result in a significant opportunity cost and show the effects of missing the one best month on an annual return. “Although successful market-timing may improve portfolio performance, it is very difficult to time the market consistently,” says Lauricella, adding that the long-term gains from US stocks have been demonstrated to offset short-term losses.

Even worse, poor market timing means you give up the chance to gain more from the compounding of reinvested gains, therefore the net effect in an investment strategy is negative when compared to a portfolio that stays the course.

What is Compounding?

In a short answer, staying the course is the key to allow the compounding to work out. But what exactly drives compounding. Let’s start with what’s known as the ‘compound interest’ formula:

End value = Initial value of capital*(1+Rate of change)Time

- Initial Capital determines how much in absolute terms you can gain at a certain rate for a period of time.

- Rate of Change or the rate of investment return defines at what pace the initial and reinvested capital is to compound.

- Time Horizon defines for how many time periods your assets compound itself.

Put simply, compounding can be explained as the money (or returns) your portfolio earns each year, and then both your initial capital and your returns of previous years earn returns, leading to a point where you have a much larger capital pool. That means, the larger each of the equation’s components (on the right) is, the bigger your total capital would snowball into overtime.

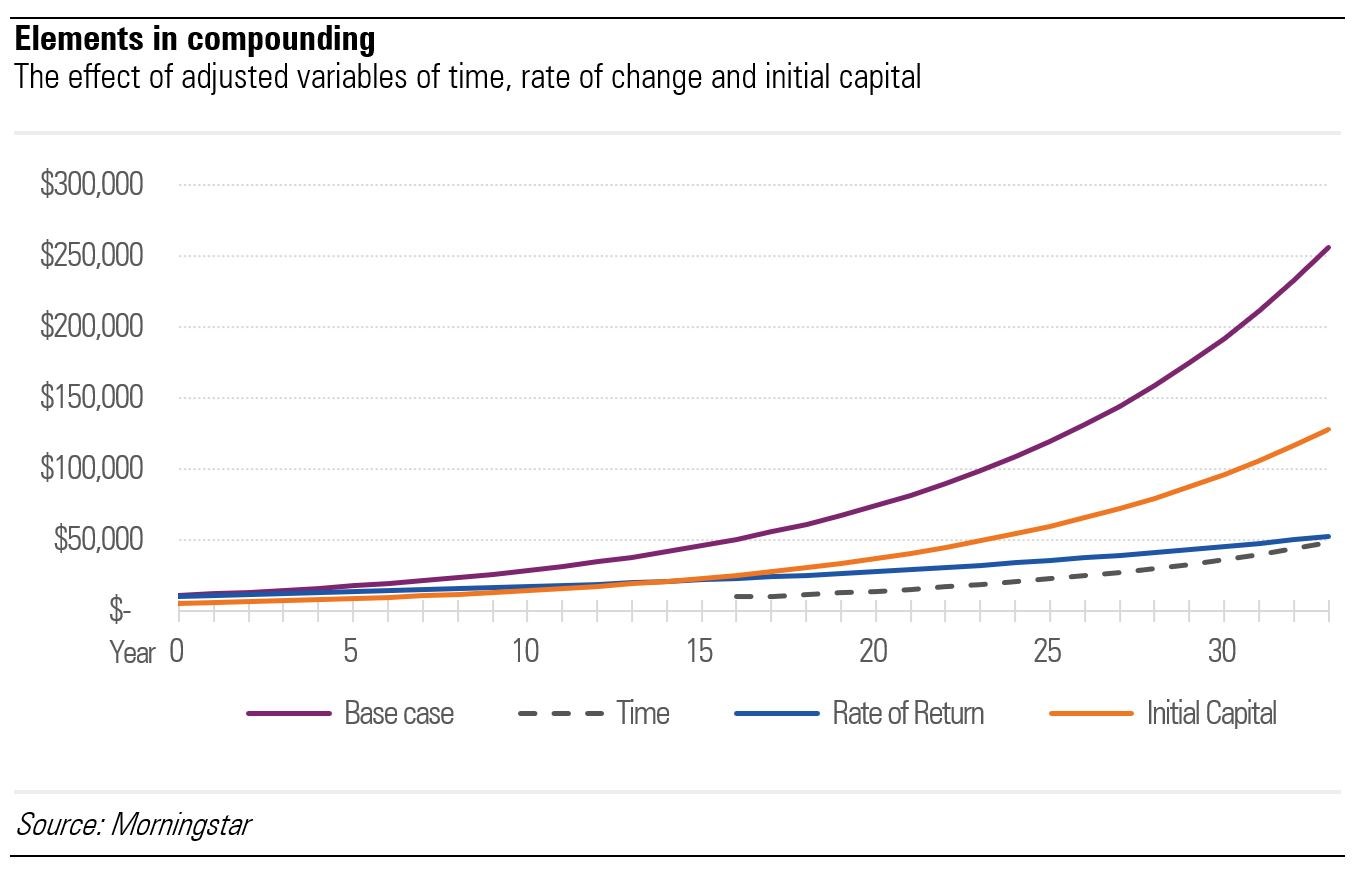

It’s clearer in a side-by-side line graph that plots four scenarios. First, we let the base case (purple line) be a portfolio with a starting capital of $10,000. The portfolio invests in assets at the end of Year 0 that could generate an average of 10% each year and remains the same for the next 35 years.

For each of the remaining three lines, only one variable is adjusted in illustrating the outcome upon a shortened time horizon, a lower rate of return and a smaller capital to start in the equation.

With all else equal, beginning with capital in half means the portfolio will grow at the same rate but arriving at the exact 50% in the end value of the base case.

By contrast, when axing the investment horizon and the rate of return by half, what you afford is a return far less than just half of the base case. Shortening the investment horizon gives up the sessions that the portfolio can compound, while a smaller investment return simply flattens the curve by a large extent. Both result in merely 20% in end value as compared to the base case.

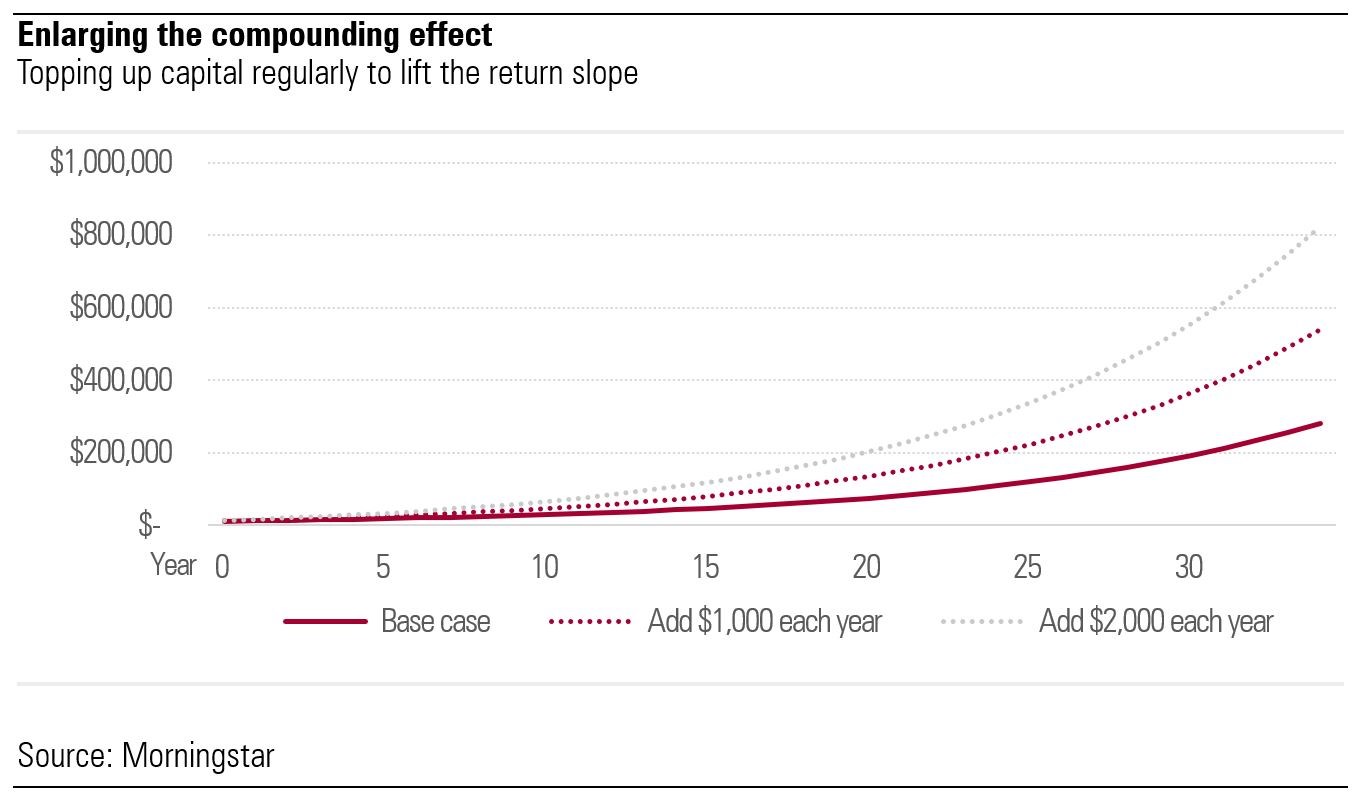

With a view to long-term performance, we go back to the base case of our data simulation and assume that in each calendar an investor adds 10% and 20%, in this case $1,000 and $2,000, to their portfolio (shown as dotted lines).

We find that upsizing the total portfolio value on a regular basis takes advantage of the compounding, enabling the portfolios to notch high absolute returns. This is for those who don’t have a large pot of starting investment capital, say at the early stage of their careers. Instead of sitting on cash to save up a sizable amount in some time, it is worth considering starting small to let the compound work. Expanding the capital base can come later by building up a disciplined top-up mechanism to your portfolio.

Indeed, the stock market is seen as a risky investment if you look at it for the short term. Data have shown proof that long-term returns have outsized short-term fluctuations and have triumphed over the risk of missing the one best month on an annual return by betting in and out. In practice, trying to call the trough and the peak of the market prices is distinctly tricky. The strategy involves a great deal of knowledge and luck. For individual investors who lack experience and time in technical research analysis, market timing would then be primarily driven by biases like loss aversion or herd mentality, which may cause some investors to end up buying high and selling low. Staying the course will bear fruit if you endure the time with discipline.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")