Chinese automakers are flocking to the crowded electric vehicle arena. For companies in the space, simply news of forming partnerships with tech companies in developing smart cars and autopilot would have pushed up share prices. But Morningstar analysts warn against buying the euphoria, citing a handful of issues facing traditional carmakers that investors shouldn’t ignore.

One important reason to avoid Chinese carmakers is that they have no economic moat, or competitive advantage. This comes with their innate features shared with most auto companies globally:

- The industry is capital-intensive, but barriers to entry are not as high as they were in the past.

- Automakers face a great deal of competition so gaining a sustainable advantage is nearly impossible.

- Auto demand is cyclical. Even the best automakers cannot avoid downtime and a large drawdown in return on invested capital and profit.

- Money can’t buy brand image. The best ones are at least 100 years old. (Tesla (TSLA) is a rare exception).

“For the past 50 years, automakers worldwide generated a median return on invested capital of less than 10. Only BMW and Ferrari are the exceptions that consistently earn above the cost of capital returns over the next decade,” says Ivan Su, equity analyst at Morningstar Asia.

China autos struggle with issues other than the classic ones.

“With its relatively short history and limited landmark models, it’s difficult for homegrown Chinese brands to compete with foreign brands domestically and extend its reach to overseas,” says Su, who believes the addition of EV to the market will complicate the already-competitive scene.

Legacy Haunts State-Owned Enterprises

Historically, autos and engines are closely associated with military use. National security concerns halt the entrance of foreign players in the industry. China which has a long history of subsidizing maiden motor technologies and protecting them from the competition. One measure taken was forbidding foreign brands from solely operating in China, but the rule will be lifted by 2022.

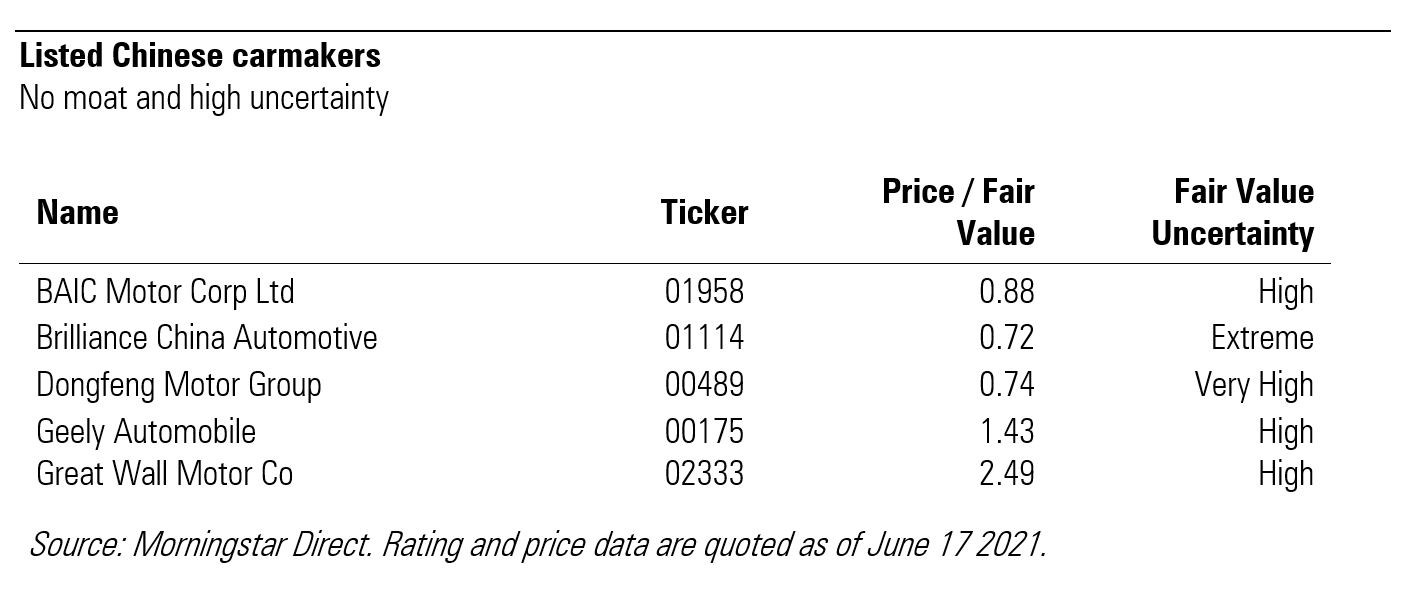

Looking in the rear mirror, such regulation grew several state-owned players, and their control over the profitable joint ventures with foreign partners has been the source of profit. BAIC (01958) is the parent company to a JV with Mercedes Benz and Korea’s Hyundai (005380). BMW entered the market with Brilliance (01114) and Dong Feng (00489) is a partner with Paris-listed Peugeot (STLA).

At the same time, partnership with formidable foreign companies has reduced to a large extent the motivation for Chinese companies to develop and enrich their own car fleet. And this creates a lasting problem. “As the ownership rules loosen, the foreign partners are expected to take a larger share in the JV entities. We see no visible signs Chinese brands have significant and sustained edges left,” according to Su.

EV Imagination Drives Up Multiples

Over to the non-SOEs, Great Wall Motor (02333) and Geely Automobile (00175) are in slightly better shape but are still considered weak players on a global scale. They have rather lean production lines and operate in the Chinese middle-class market where customers are known for their lack of brand loyalty.

Another reason that the two names aren’t a good buy right now is their valuations. Currently, Great Wall is trading more than double its fair value and Geely is 43% above fair value. “The market pays up an exaggerated multiples for the aggressive imagination in developing electric vehicles and autopilot technologies.”

To put figures into perspective, Great Wall and Geely have initiated its own innovative product lines. Geely runs a low-margin EV segment but limited disclosure from the company is available.

For Great Wall, its EV business started roughly three years ago. Today, 7-8% of its sales are generated from EVs. “The margin remains quite low and we don’t see it near to breakeven,” Su says. “We reckon that Great Wall is also committed to developing autopilot technology but depending heavily on the third-party supply. Key components, like cameras and sensors, are sourced externally. Thus we believe that its early-mover advantages may be easily weathered.”

As a broader carmaking industry, competition is increasingly intense. “Investors should not rule out the likelihood that mainland Chinese buyers will go for EVs made by pure-play EV makers, like Tesla, or even domestic start-ups NIO Inc (NIO) and XPeng Inc (XPEV).”

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")