China equities have not been able to replicate the impressive performance of 2020. Stocks have been heavily beaten down because of the sweeping rules imposed on several key sectors. First, the antitrust fine on Alibaba Group (BABA), then the data privacy investigation on Didi Global (DIDI) and most recently the reforms that upended the profit generating after-school tutoring segment.

Fears quickly spread, and investors are dumping shares across the board, including names that are expected to enjoy better competitive advantages even under elevated competition and stricter scrutiny. In this environment, steering completely clear of a drawdown is impossible.

In Hong Kong, there are 130 funds investing in mainland China, Hong Kong and Taiwan companies for sale. They generated an average loss of 4.6% (proxied as Global Category of Greater China Equity) between January and July 2021. In July alone, the average fund performance was a negative 9.4%.

Germaine Share, Director of Manager Research at Morningstar says a short period of poor performance isn’t enough to justify the decision to withdraw from the fund units.

“Selling the funds after months or just weeks of a poor performance means giving up the opportunity for the market or the portfolio to recover. At the same time, this would imply locking in those losses right away.”

Know the People and the Process

To evaluate whether you should hold on to a fund, consider the Morningstar analyst rating methodology. “First, we look at the People pillar. We believe that fund managers and the management team in the industry over longer stretches of time would have experienced different stages of a market cycle,” Share says.

Another pillar is Process. Clearly defined and repeatable investment processes warrant better ratings and investors would have higher confidence in managers that stick with the stated investment objective. Funds in the same category come with varying investment styles, but a good manager should stick with what the status documents promise.

Share explains with the example of a specific stock. In 2020, an exposure to Meituan (03690) explained part of the return differences across the China equity fund category. Before the pandemic, not all equity managers were convinced of the potential of the food delivery services provider. But once the pandemic hit – and the share price rallied – some managers decided to enter the stock despite a lack of conviction.

“We raise yellow flags for managers who decide to chase good performance -- like Meituan in 2020 -- just to catch up with the boom. We take comfort in a manager that is sticking with an investment strategy, even though that may bring their portfolios a certain level of detraction from returns. This shows that their calls come with solid reasoning.”

Downside Protection

It’s not just performance chasing, investors should not overlook managing risks in the portfolio. “Mutual funds are professionally managed by asset managers. Compared to doing-it-yourself, and betting on single stocks, a professional approach is better in two ways: the access to investment research that help generate stock ideas and the risk management framework and tools,” Share explains

“Notably, the investment framework usually comes with the restriction of single stock or single sector weighting. This mechanism protects investors from being too concentrated into one sector, or in an extreme case one stock,” she adds.

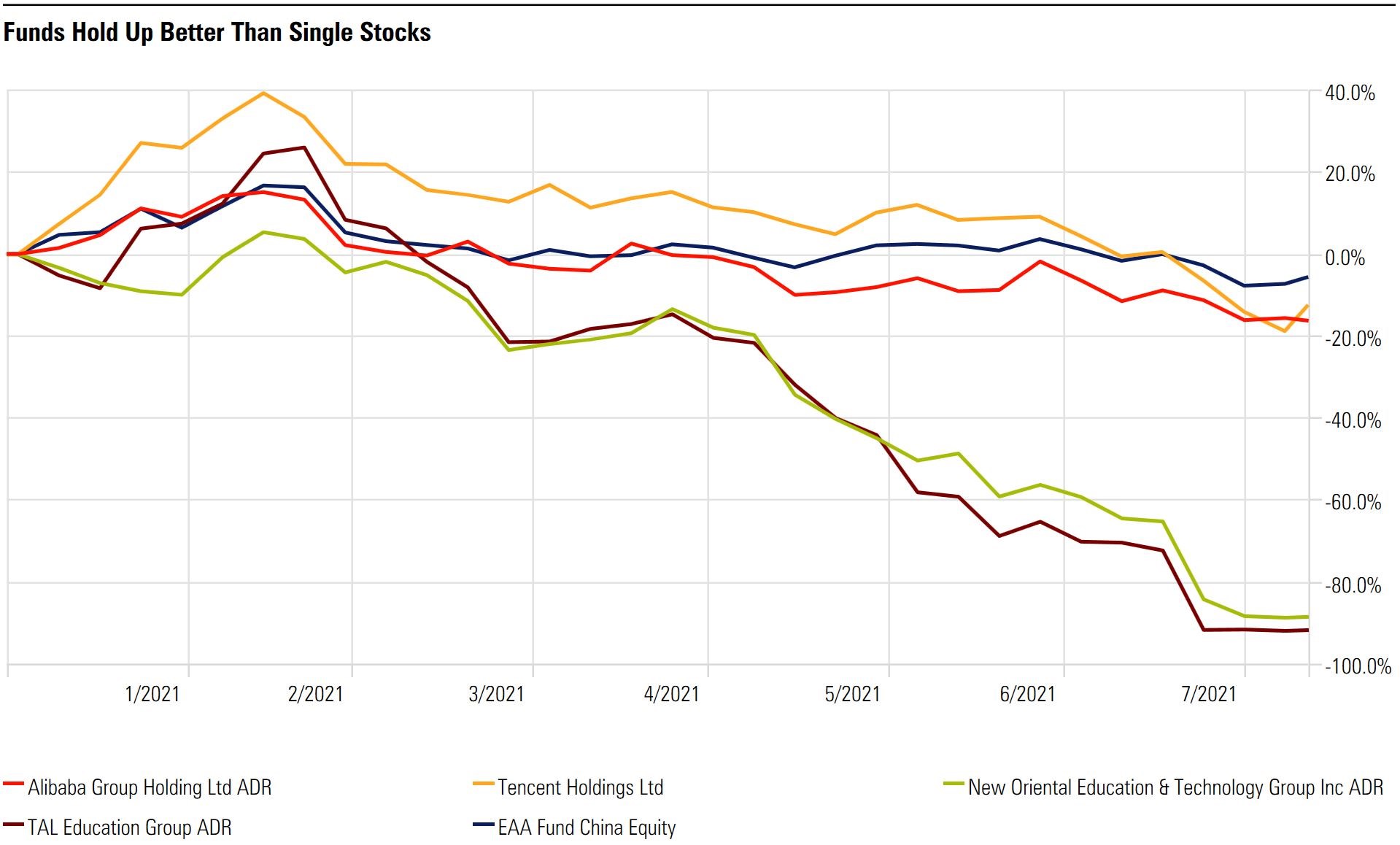

If investors are looking at fund performances from a relative perspective, multiple holdings tend to cushion losses when one or two stocks take a plunge. Since the beginning of the year, Greater China equity funds have been holding up well.

According to Morningstar research, the recent underperformance of China-focused funds is in line with expectations, given the names that came under the regulator’s watch happened to be the big index constituents. As of the end of July, Tencent Holdings (00700) and Alibaba Group represents 14.1% and 12.7% of Morningstar China Index, respectively.

Expect More Regulation

Lastly, specifically for China, the huge market still carries the nature and feature of an emerging market –progressive development would continue leading to regulatory improvements, says Wing Chan, Director of Manager Research Practice, EMEA & Asia.

Every few years, China enters a policy cycle aiming to rectify industries that are critically important to society and/or the economy. For example, overcapacity in raw materials was a major issue in 2016. In 2018, the Chinese authorities shifted focus to prioritize the quality and the supply of medicines. He adds: “Regulatory risks could still be in part of the market. That said, when we look at the risk-return rewards in the Chinese capital markets, they are by far a good place to find excess investment returns.”

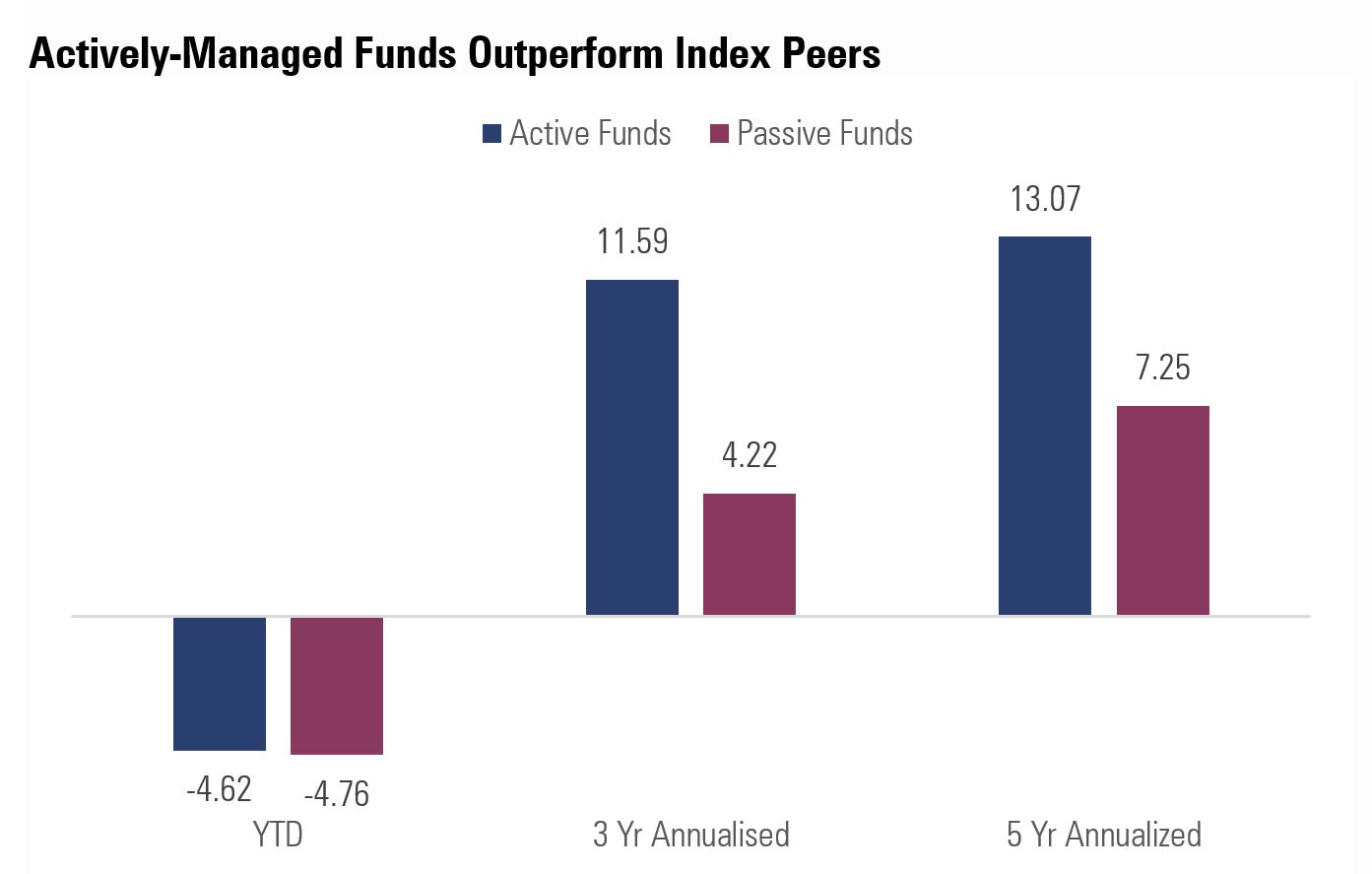

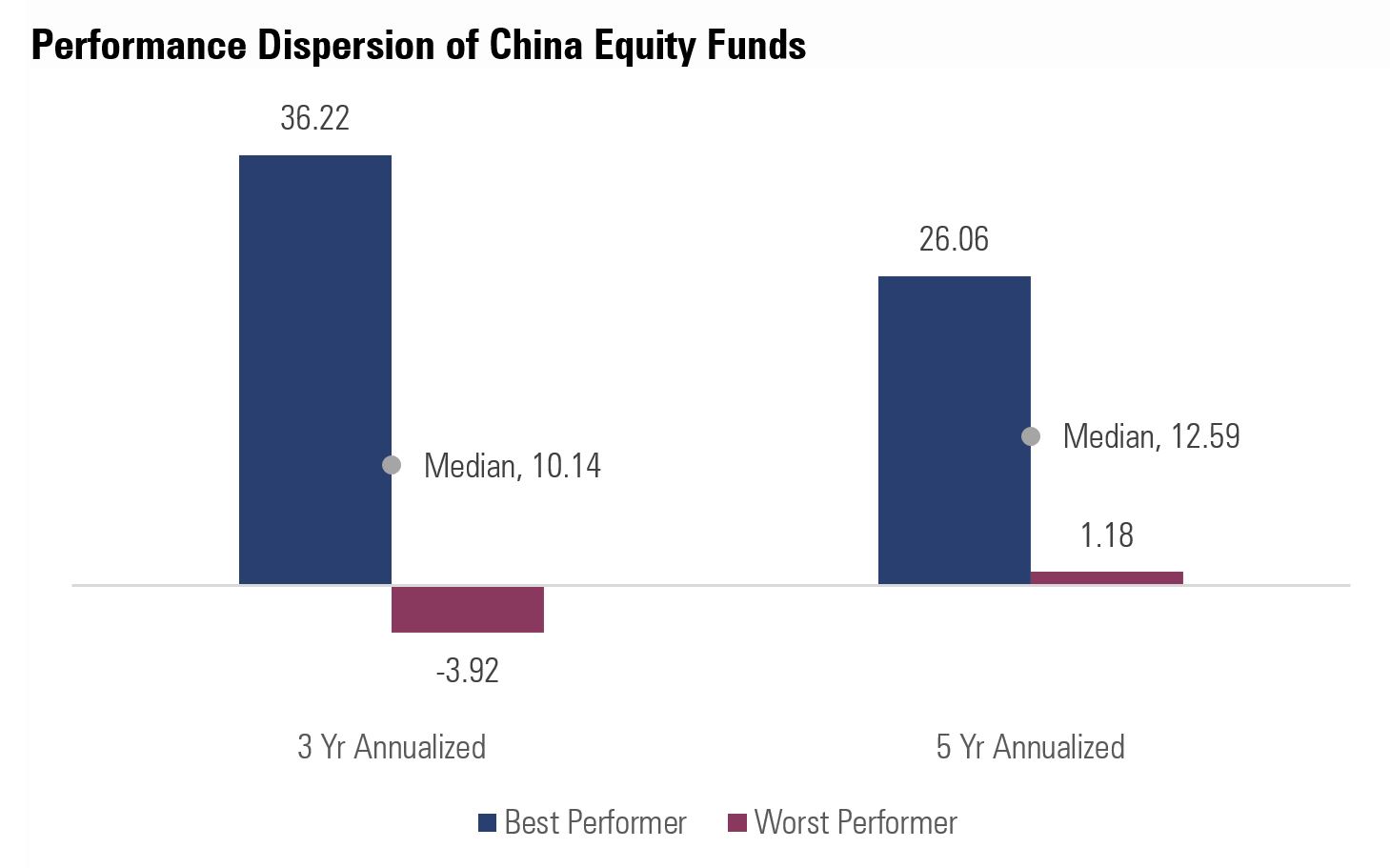

Interestingly, this environment continues to amplify some extreme dispersions between top and bottom performers and ultimately favors actively-managed funds. “This echoes the importance of stock picking skills and quality of a fund manager,” Chan concludes.

Morningstar analyst ratings for mutual research is a long-term recommendation produced following the methodology proves to set apart alpha generators through market cycles of three to five years. We rate a total of 13 Greater China Equity funds in Hong Kong.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")