In a move that could change the very identity of Macau, one of the world’s biggest gambling hubs, the local city administration initiated a consultation that suggests an increased scrutiny of the region’s casinos.

The Macanese government released a document up for public consultation that looks to appoint government representatives to “supervise” companies and increase local shareholdings in casino operators. Additionally, companies will need “official approval” before distributing profits such as dividends.

Jennifer Song, senior equity analyst at Morningstar, lists three major takeaways from the 45-day consultation:

- First, the proposed revised gambling law will set up scrutiny of casino operators and increase local ownership, which suggests more direct government supervision on gaming companies’ operations.

- Second, China’s crackdown on cross-border currency outflows and money laundering spells likely risk to junkets and the VIP segment.

- Third, there is little transparency on the renewal of gaming licenses, with little guidance so far on the number of licenses and the concession period, as well as restriction on capital allocations.

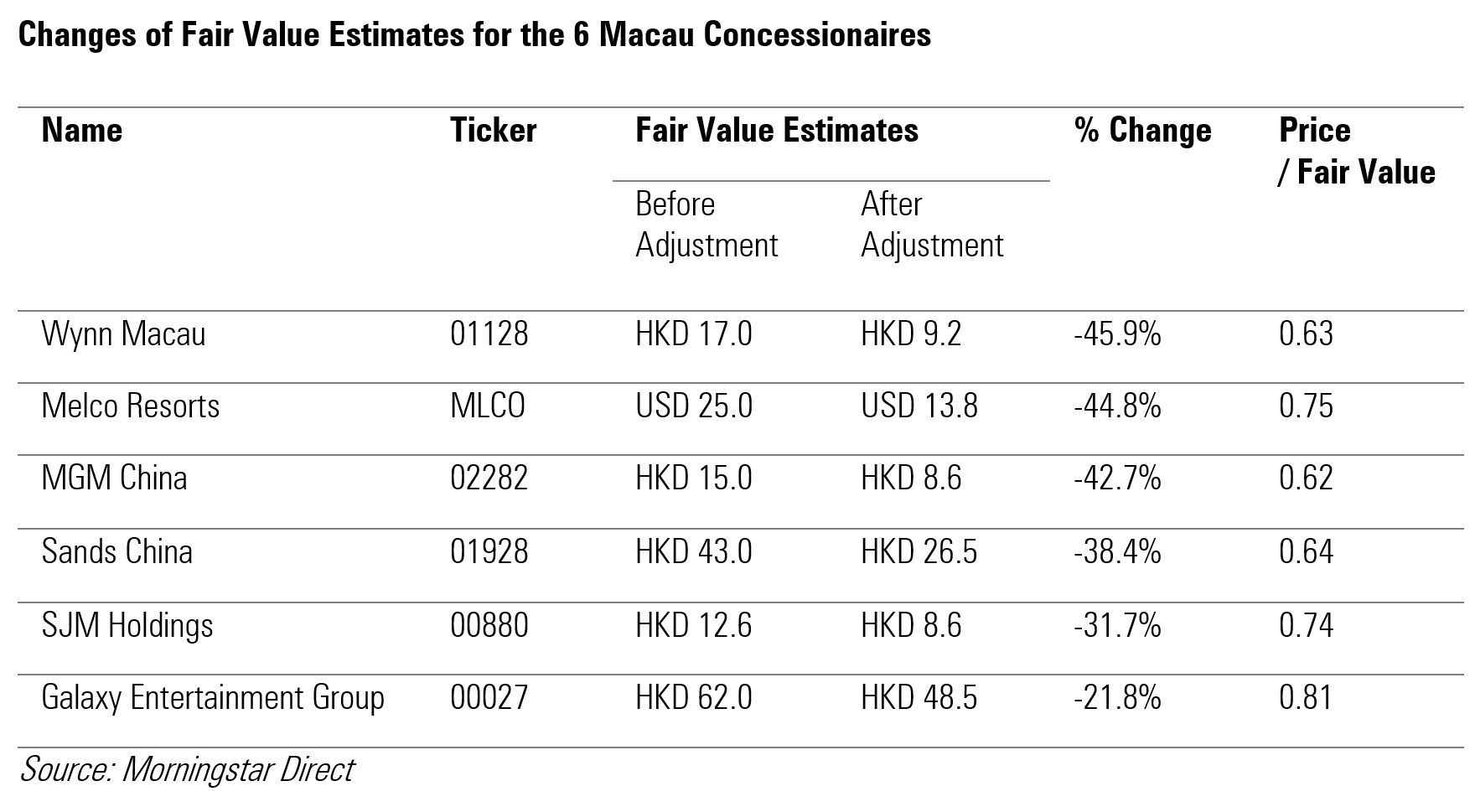

Fair Value Adjustments

Due to the reduced visibility in the long-term business outlook for casino operators, Song adjusted the fair value uncertainty rating for the Macau gaming companies to ‘very high’ from ‘high’. For the six active license holders, Morningstar analysts assigned a 22%-45% trim in their fair value estimates.

Riskier U.S. Operators

The possibility of losing the licenses for these foreign-owned casinos remains low as new concessions will have a destabilizing effect on the industry profit pool, the taxation income that it generates, and the knock-on effects on the social policies of the mainland government. It is possible that the concession allocation process is delayed ensuring the financial solvency of the operators during the pandemic, and Song would expect an extension to current concessions to be made in this case.

But in Song’s view, operators with a U.S. background may be impacted more than the local peers on the direct supervision front. Wynn Macau and Sands China are the arms belonging to their respective US-based parents, Wynn Resorts (WYNN) and Las Vegas Sands Corp (LVS).

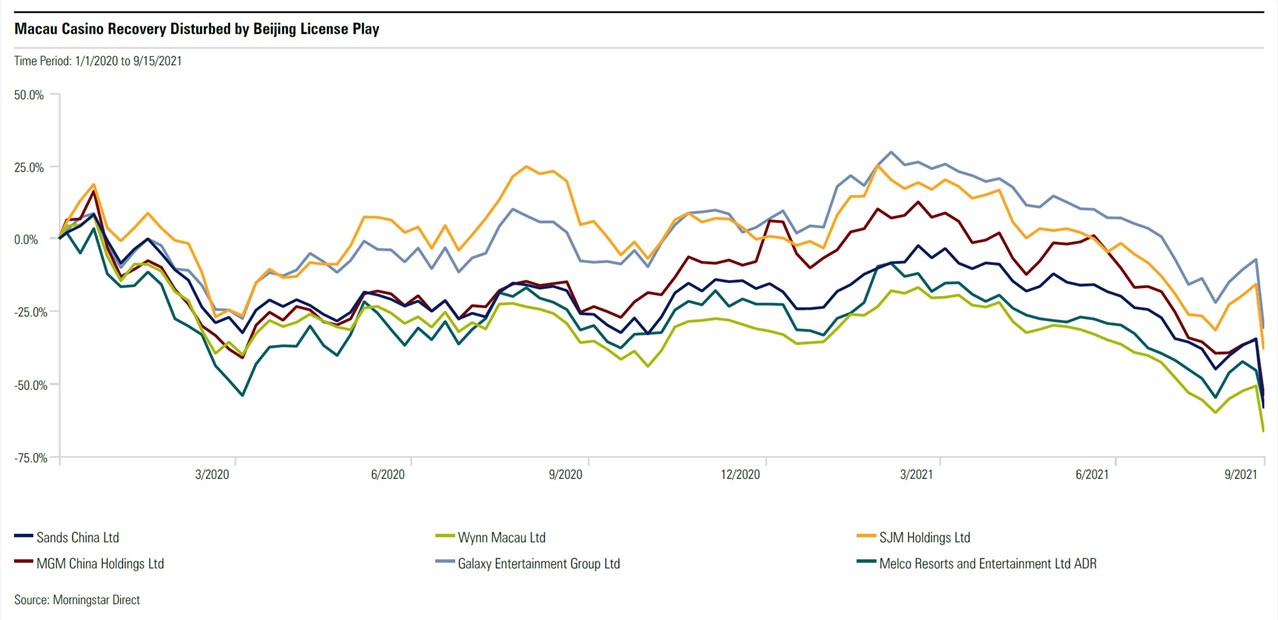

“The policy steer is fairly vague but the reference to social responsibility is sending chills down the spines of investors, given recent developments in the technology and education sectors in China, and represents a major new source of uncertainty,” explains Song, on the immediate share price slump for all casino operators. The market sees the regulatory implications as being more severe than what a pandemic lockdown would bring. Shares in casino players are now beneath the lows reached in March 2020 at the height of the COVID outbreak in China.

Gambling on the Future

Despite a considerable trim in her fair value estimates, Song still takes comfort in the Chinese government’s will to anchor Macau’s position as a world-class center for tourism and entertainment. But the focus of the sector must change. “We expect a wider effort to be in place to discourage junkets, in order to quicken the transformation of the sector’s revenue mix. Going forward, the casino operators will have to lean toward the mass market and their nongaming contribution for growth, rather than the high rollers.”

She stresses that the policy isn’t new. The central government has been taking aim at junkets and hoping to improve the entire landscape of the gaming industry. This is also to keep up with Asia’s gaming regulation standards. Junkets are known as the middlemen who solicit high rollers to gamble at a casinos VIP rooms.

“China has been clamping down on activity by VIP punters in Macau over the past years, which could sometimes be an illicit channel for currency outflows and money laundering, as well as cracking down on organized gambling trips to Macau and other overseas destinations by junkets,” she explains. The client mix will have to be fine-tuned but a complete wipe-out of contributions from the VIP segment remains a low probability outcome.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")