Earlier the month, electricity was rationed in China, impacting industrial powerhouses such as Guangdong, Jiangsu, and Zhejiang, among other provinces. While electricity curtailment is not that unusual for China, this time the pandemic played a part in powering the power cut.

Why Was There a Power Cut?

Morningstar’s equity research team identified two reasons for the urgent blackout.

First, stay-at-home orders during the pandemic meant that consumers turned to buying goods instead of traveling, dining, and other services. As most manufacturing production lines were shut under lockdowns, the early containment of COVID-19 in China made the country a perfect location to pick up unfulfilled orders. Our analysts see the sharp turnaround in Chinese export figures as evidence of this. As manufacturing plants filled capacity, China’s power consumption also posted sequential growth.

According to Morningstar’s estimates, the growth level was between 5% and as high as 25% during the period. Subsequently, although many of the economies reopened their orders, the arrival of the Delta variant sustained China’s role as a global manufacturing hub.

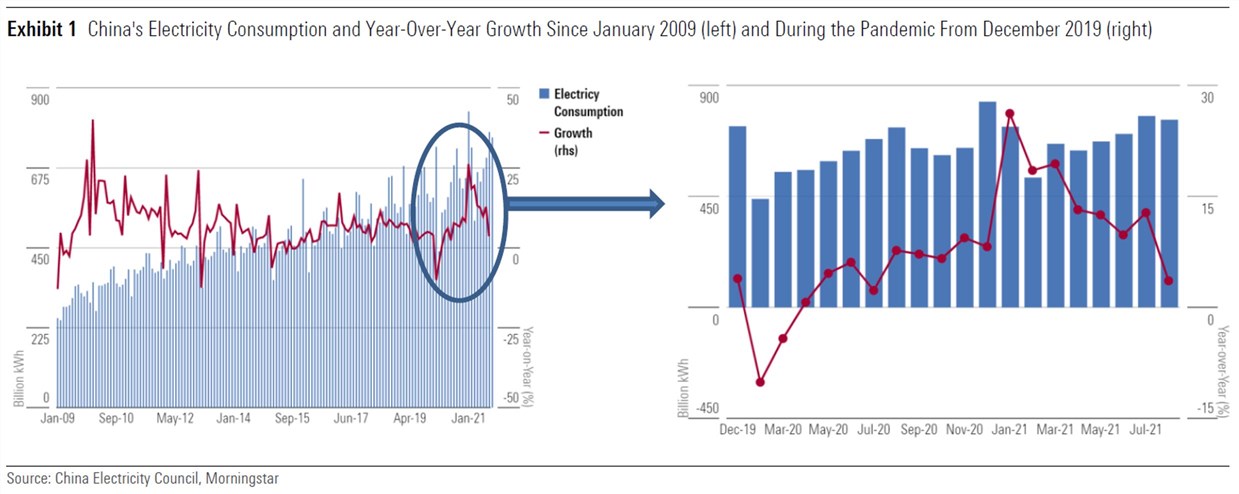

Second, to help the economic recovery, Chinese authorities took an easing approach in fiscal policy that encouraged infrastructure spending. The uptick in industrial activity also increased electricity use. Lorraine Tan, Morningstar’s director of equity research, cited the data compiled by the China Electricity Council and says growth in electricity consumption for the first eight months of 2021 has averaged 13.8% compared with the same period in 2020.

Outside of the pandemic, Tan says the country is trying to pave the way to carbon neutrality by 2060 while providing sufficient power for the economy. She continues: “Coal production in China, plus the importance of this energy source, have been largely reduced in favor of renewables. But there are seasonal factors that impede some renewables.” So far this year, hydropower output is down 1%, affected by very low water flows. Moreover, the mismatch of power demand and supply on the mainland was pulled further by seasonality.

What is the Likely Domestic Impact?

From the channel checks conducted by the Morningstar equity research team, most of the power shortage will have a temporary impact, mainly from the global supply bottleneck triggered by pandemic-related disruptions.

Another near-term factor is Christmas. This is a typical period where production capacity will have to be filled to meet the festive orders shipped between October and November. After that, pressure on the power supply-demand dynamic would ease. Tan says that logistics-related demand will also push energy prices higher, alongside an increase in crude oil prices. “The good news is that we think this will only last through to the Chinese New Year period, and we think that the impacts will then diminish,” she says.

As winter approaches, demand for air-conditioning will reduce, especially in South China. Moreover, Tan foresees the winter in the Northern part of China will be harsher, pushing up natural gas prices.

What Does the Power Shortage Mean for Investments?

Tan says most of the companies under Morningstar’s equity coverage report a low level of direct impact from the power cuts. She adds: “But, obviously, companies that have utility as a big portion of their costs are going to be sensitive to rising energy costs over the next six months.”

As Morningstar analysts find, the surging cost of coal does filter through to the overall energy input costs, including LNG. Natural gas normally turns more expensive during the winter months in China, or between mid-November and mid-March.

She explains that an increase in overheads may risk margin compression over the next nine months to a year. “Coupled with a still very tight supply chain, the rising energy cost will lead to higher input costs in terms of hard and soft commodities as well. It would not be surprising to see some risks of margin compression across a few sectors,” says Tan. The food and beverages, heavy industries, such as building materials, and energy space may see pressure. Thus, if these companies are unable to pass on higher input costs to consumers, their earnings will see temporary margin compression.

.png)

.jpg "Kate Lin")