The Chinese regulators set the tone on industry reforms in 2021, starting with a months-long regulatory crackdown, which caused investors at home and abroad to lose confidence in the market. This in turn catalyzed selloff in mainland companies.

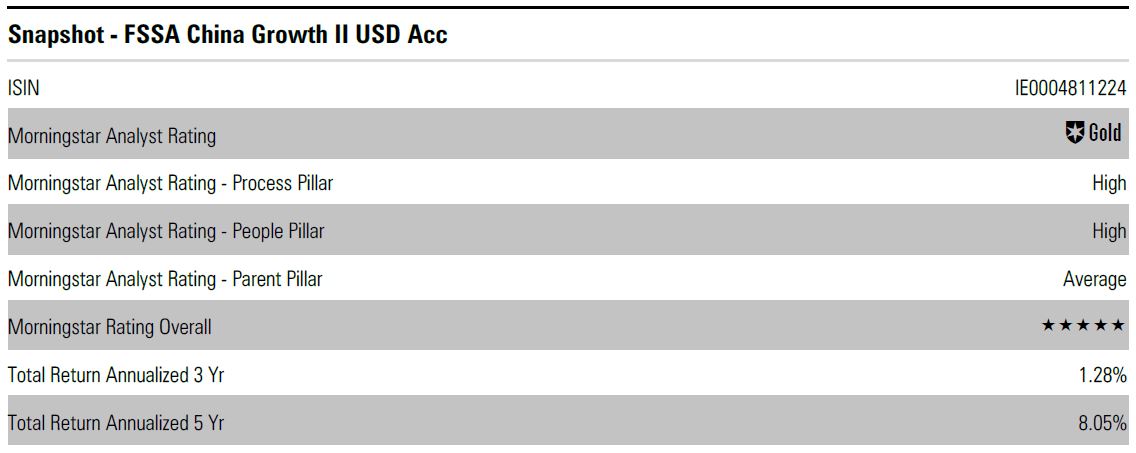

While the struggles facing Chinese equities continue to dent market sentiment, Martin Lau, lead portfolio manager of Gold-rated FSSA China Growth Fund, believes that, in the long-term, focusing on investing in the highest quality companies in the region will generate attractive risk-adjusted returns for investors. The medalist manager finds some of the more expensive, over-valued, over-crowded sectors to be “vulnerable.”

Doesn’t Pay to Follow the Crowd

The market’s herd-buying mentality is never a proper indicator of investment value, Lau says. But the question is, how can investors justify the investability of a sector or even a single name? The first tactic is to stay away from what’s called the feeling of FOMO (fear of missing out) and always analyze and judge whether the reasons that attract the market’s hype are legitimate or not.

Instead, a sudden surge in investments has been a red flag to long-term investors like FSSA Investment Managers.

Take electric vehicles, for example. Lau’s portfolios have shied away from electric vehicle manufacturers. He says: “The electric vehicle rally we saw is giving investors the impression that this story is a broad success across the board – meaning that traditional car manufacturers like Ford and Toyota will be benefitting alongside electric vehicle stalwarts like Tesla. This scenario does not make much sense because people’s demand for cars would not be lifted by electrification of vehicles. Unless you believe electric car makers are more like software companies, with much higher margins, you’ll have to be extra careful making bets in the space.”

Lau took a step back and believed the current hype for electric vehicles is not an isolated case. A similar boom happened years ago in old-economy industries like producers of steel and cement. One of the more recent examples was the rise (and in some cases, the fall) of smartphone manufacturers.

Trying to Identify – and Invest in – Future Market Leaders

Even though the world is hyped to see a game changing technology in communications, not all the companies that participate can succeed – at least not to the same extent. “The reality is, Apple became the industry and technology leader, while Samsung closely followed. China’s Huawei and Xiaomi made a little money; LG withdrew, and the rest are making a loss.”

“To us, investor demand that leads to a sudden boom has been a warning signal,” Lau says.

He ties his learnings from the smartphone industry back to electric vehicles. “At this stage, there’s hardly a clear leader in this fledging industry. But the high valuations before any EV sales, and the rally in the past couple of years imply the success of multiple players, which we know wouldn’t be possible as the sector matures.”

"In these industries, when the leader emerges, it is very difficult for other companies to compete. For example, the development of a smartphone requires billions of dollars, such as semiconductors. TSMC announced that it will invest US$100 billion in research and development. If you do not have a market share and cash flow, it is very difficult to compete," he explains

How to Find Quality in the Stocks

Lau puts his focus on the people. This element is distilled from the quality of the company management and the board of directors. In his portfolio, one firm that stands out in terms of management quality is China Merchants Bank. Unlike other state-owned banks, CMB adopts the scheme that ensures independent decision making from the executive management teams. The governance structure also differs from other SOEs where a new chairman is appointed every five years. In contrast, the bank is not held to such a rule and therefore can anticipate a a longer-term run of planning, operation and growth.

Lau commented: “The Chinese banks operate under the same environment, running under the same interest rate level and loan growth. That means their financial performance and bad debt level look similar in the end. Thus, good execution and management quality would appear to be the differentiating factors for quality names in the space.”

Other than management quality, in Lau’s investment process, he also looks at the companies’ agility to changes in the market.

“As bottom-up investors, we have observed how companies navigated through various crises, such as by adopting new technologies, cutting excess costs or deploying the findings from marketing and research, and development budgets more wisely.”

Right now, the undergoing correction of Chinese stocks brings valuations down to more reasonable levels, which present opportunities for Lau’s portfolios to accumulate quality companies. Here is a list of the fund’s top holdings:

.png)

.jpg "Kate Lin")