Is there any one among us who does not want to own real estate, and make a steady income out of it? If you want to buy and maintain income properties, you’ll need lots of initial capital. But for those of us who do not have millions to spare, we can still invest and earn income from real estate – through REITs. In Singapore, REITs are a hot favourite investment. Today, we’ll answer three questions investors have around Singapore REITs.

Question 1: Why Retail REITs When There’s No Tourists?

That’s particularly true for Singapore as tourism makes up a big chunk of retail sales, around SGD 30 billion ($22.6 billion) in 2019 or 4% of its GDP. Given the current coronavirus pandemic, the return of travelers to the Lion City is likely to be delayed for some time more to come.

Though several regions, like Australia and Hong Kong, are mulling a ‘travel bubble’ arrangement with Singapore, these plans remain in a discussion phase. Australia, for instance, brought up an Australia-Singapore travel bubble in October 2020, but it has not materialized. The one connecting Hong Kong has been postponed few times due to a flare-up of COVID infections on either side since its initial scheduled launch in May. The suspension of the travel bubbles may have implications that a full recovery of Asia’s hospitality industry and tourist spending might not be close at hand.

However, retail REITs invest not only in properties exposed to international travelers, but also in those that serve domestic demand. Notably, suburban malls can target residents in the vicinity, thus having lower sensitivity to tourist arrivals.

Analysts say investing in these homegrown malls should make a strong case for the medium term. With the economy turning for the better, low unemployment, moderate inflation growth and rising personal income are expected to underpin retail sales growth.

Question 2: Does WFH Kill Office Needs?

Offices have been asked to move back to a work-from home status and the market has concerns that large banks such as DBS, Standard Chartered and OCBC are looking into reducing their office space needs.

Morningstar analysts see this having a more limited impact, given the early signs that office rents and occupancy rates in the core central business district begin to stabilize in the first quarter of 2021.

This is because most potential tenants are taking a longer-term view to their office space needs and the lack of new supply should allow the space coming to market to be absorbed. Citing Keppel REIT and CICT, Lorraine Tan, Morningstar Asia's Director of Equity Research says their office spaces are seeing decent enquiries with global technology companies looking to expand in Singapore.

Over on the supply side, near-term office rental still sees support from a tight supply especially in the central business district through 2022. New office space won’t be available until 2023 as a large supply of 1.3 million square feet and 1.0 million square feet is to be added in 2023 and 2024, respectively. Tan expects that by then growth. in office rentals will be rather muted.

Question 3: Are S-REITs Sensitive to the Current Pandemic Development?

Comparative to all REIT types, those holding retail properties are most affected by stricter social distancing measures, such as the move to close indoor dining, as this hurts restaurants and other such services. However, though these rules can adversely impact the already weak retail sentiment, businesses and customers are better prepared now than they were during the first stages of the outbreak.

Also, Singapore has begun relaxing its social distancing curbs. Tan says less public panic in this round of circuit breaker supports a quick turnaround to business activities. “Once food and beverage outlets resume in-premise dining, activity levels should rebound quite quickly,” As a whole, S-REITs pulled back on the comeback of COVID spread but she sees it a buying opportunity into selective REITs.

“Over a longer term, Singapore’s relatively high vaccination rate at 23% (two doses) points to a decent bet that we should see a relaxation in measures at the least by August. We also believe that if the measures are extended beyond the one month, government relief is likely.”

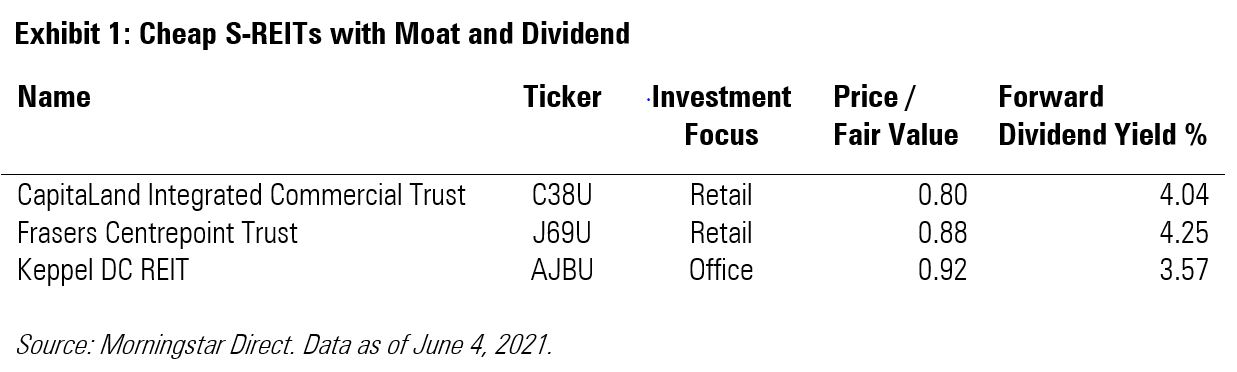

Below is three S-REITs trading at a discount to their respective fair values assigned by Morningstar analysts. They also come with a standard capital allocation rating and a stable fair value uncertainty.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")