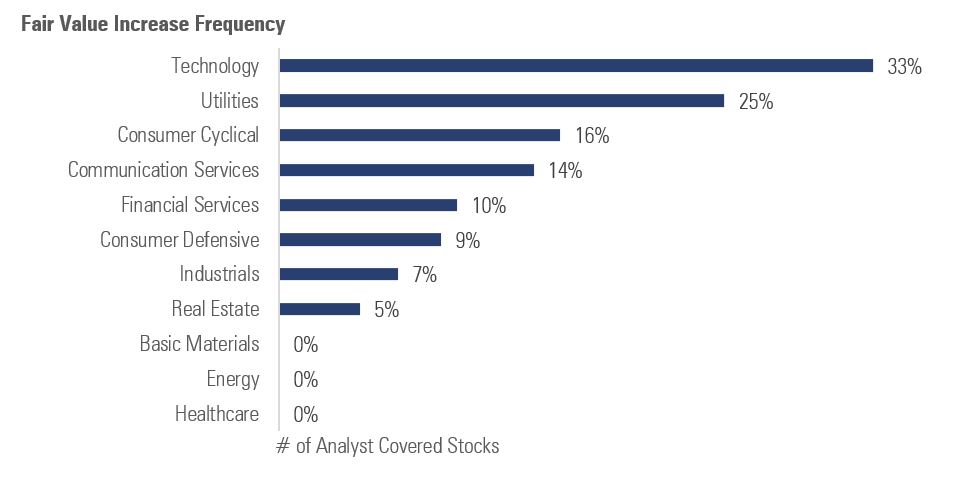

At Morningstar, increases in fair value estimates for companies across Greater China were at a slower rate in the second-quarter earnings season compared to the previous quarter.

Some may think this is because of volatility and uncertainty around the Chinese regulatory landscape, but this is not the case. Morningstar equity analysts conduct fundamental analysis and create a financial model to determine a company's intrinsic value and a fair value for its stock. While our analysts stick to a long-term approach to investing, they monitor quarterly earnings results and other factors to update their assumptions and potentially their estimates.

Between June and August, only 18 names received a 10% increase, with one-third of them coming from tech hardware-related companies, followed by two from utilities and another two from consumer cyclical. From Feb to May, 38 companies receiving an upward adjustment of 10% in their fair value.

Leaders of the Pack

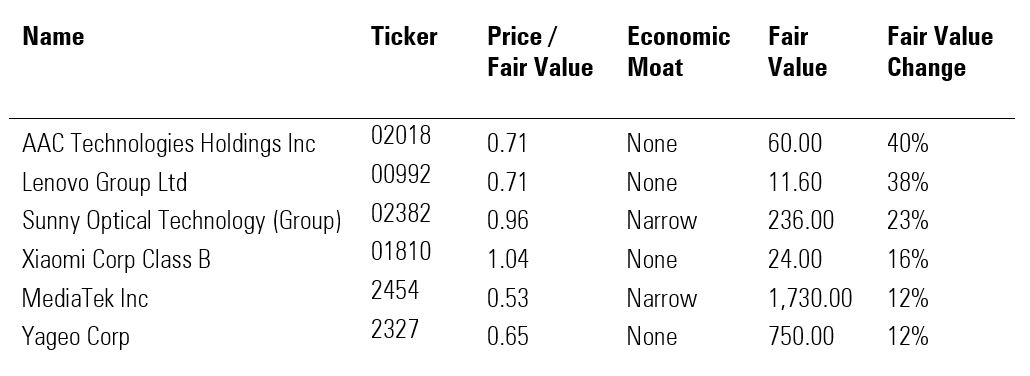

Tech leads the pack in terms of fair value increases. One-third of our technology coverage received an increase of more than 10%. Here’s the list:

The demand for PCs is to last longer than expected in the post-pandemic environment, benefitting companies like Lenovo Group (00992), which has an ideal mix of computer products, from high-end gaming PCs to enterprise devices. Our analysts also highlight Taiwan-listed Yageo Corp’s (2327) participation in EV battery chemistry as it is known for supplying multilayer ceramic capacitors, a component that regulates any electronic devices’ current flow. Sunny Optical (02382) is positioned to capture benefits from both the anticipatory upgrade of smartphone cameras in 2022 and the lens installed for auto-pilot purposes.

While the managers’ favorite, foundry TSMC (2330) is inching closer to its fair value, investors can eye chip designer MediaTek (2454) as a semiconductor play with deep value. Phelix Lee, Morningstar’s equity analyst, set its fair value at NT$ 1,730, following an upward adjustment of 90% and 12% respectively after the first- and the second-quarter earnings announcement.

Sportswear Demand Chain

Supplying for global apparel giants, and catering to Chinese nationals’ preference for homegrown consumer brands consumer sports apparel companies saw a boost.

Inking order contract with global leading sportswear brands brings Shenzhou International (02313) into light. In addition to the existing production relationship with Nike, Adidas, Puma and Uniqlo, the refreshed fair value of HK$ 171 (+71% in three months) is to reflect the signing of Lululemon as client. ANTA Sports (02020) leads an entirely different path. The company uses acquisition strategy to maintain a diversified portfolio of premium sportswear and sports equipment brands. The rich brand portfolio earns the firm a 57% boost to its fair value over the past three months.

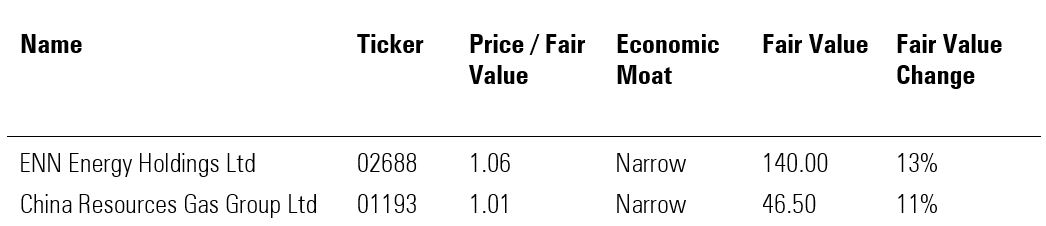

More Gas

Unlike the increases in the tech and sportswear sectors, the fair value increases in utilities were more driven by Chinese government’s long-term vision to lift gas usage.

ENN Energy (02688) and China Resources Gas Group (01193) are among the beneficiaries to ride on China’s pledge to reduce pollution by increasing gas usage to 15% of the country’s energy sources by 2030, from below 10% currently. Chokwai Lee, senior equity analyst, says the policy will underpin the long-term demand growth for gas. “We expect to see strong recovery in natural gas sales given that negative impacts from COVID-19 have waned,” says Lee, adding that both companies posted a strong second-quarter earnings. As a result, shares in both companies received a raise of around 10%.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")