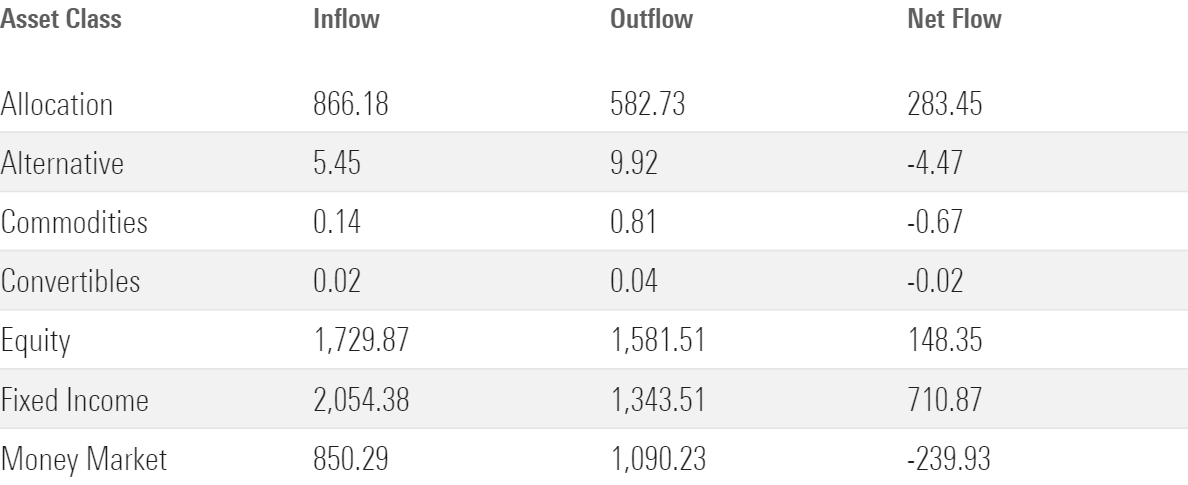

Based on the data submitted by the participating members of the Investment Management Association of Singapore, or IMAS, the various authorized and recognized unit trusts registered for sale in Singapore posted net inflows of SGD 897.58 million for the first quarter of 2023.

Breaking down the data by asset type, all three major asset classes reported inflows, with fixed-income funds seeing the most net subscriptions, which totaled SGD 710.87 million. Allocation funds saw net subscriptions of SGD 283.45 million for the quarter. Equity funds posted inflows of SGD 148.35 million.

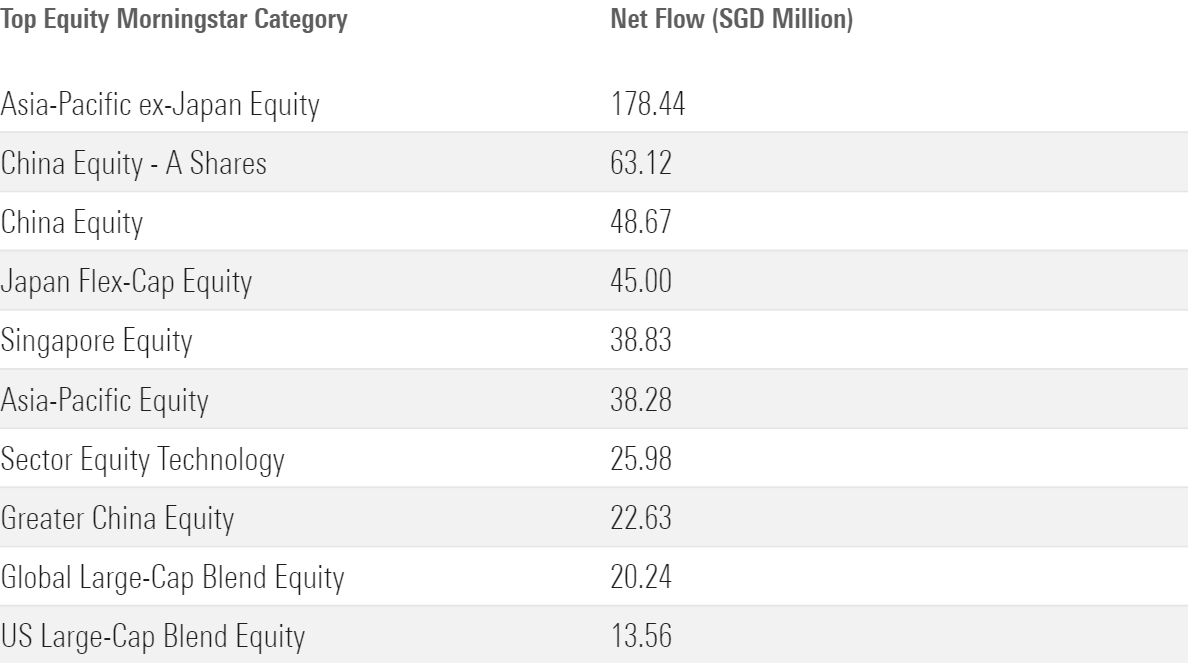

Net Subscription to Equity CPF Funds Totals SGD 148.35 Million

Major global stock markets closed the first three months of 2023 with broad gains. The Nasdaq Composite led the board with a 16% rebound. Euronext Paris CAC 40 and FSE DAX, the benchmark indexes for France and Germany, respectively, were also at the top of the chart with double-digit gains. These two European markets were closely followed by Taiwan’s TSEC TAIEX PR TWD, up 12.24%.

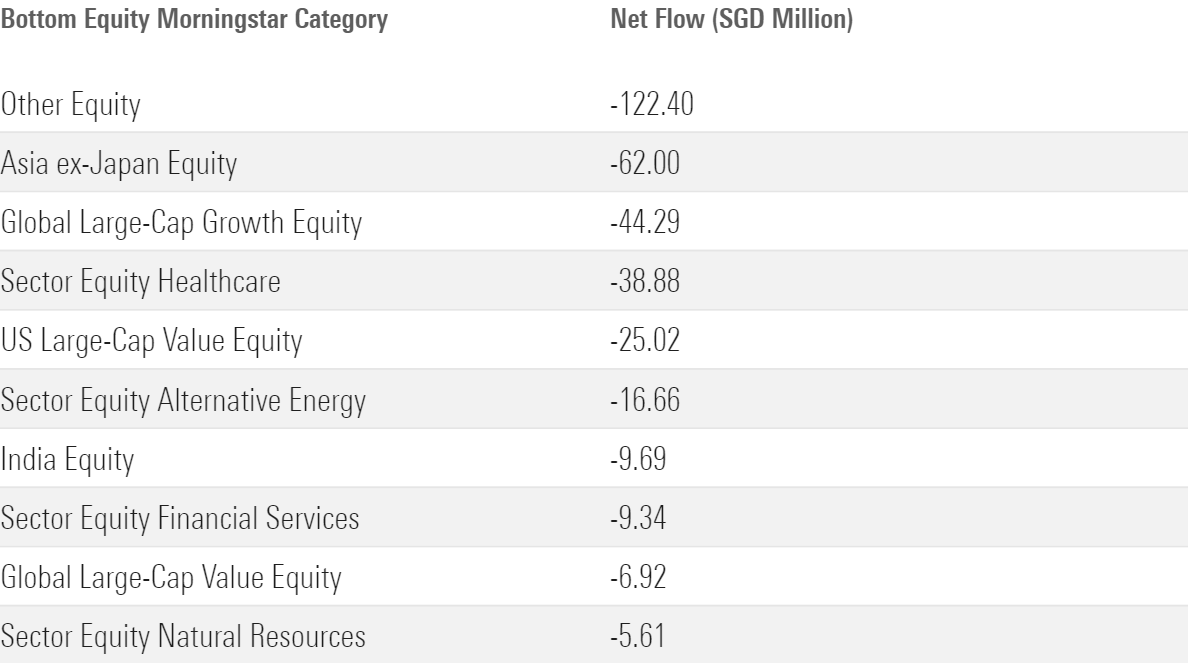

United States:The market’s focus was initially on the Federal Reserve’s next moves in tackling the uncomfortably high levels of inflation and a red-hot job market. As the quarter headed into its final days, the collapse of Silicon Valley Bank stirred concerns about a credit crunch and investors’ focus shifted dramatically to the health of the banking sector. Global large-cap blend equity funds and U.S. large-cap blend equity funds ranked ninth and tenth, receiving net inflows of SGD 20.24 million and SGD 13.56 million, respectively. Among global strategies, large-cap growth equity funds posted the biggest outflows for the quarter. Investors also redeemed capital from value-oriented global and U.S. strategies, however. U.S. large-cap value equity funds reported outflows of SGD 25.02 million while their global counterparts reported mild net outflows of SGD 6.92 million.

Europe: In this volatile quarter, tech stocks were the outperformers, rallying on better-than-expected earnings results and demand, effective cost-cutting strategies, and enthusiasm for artificial intelligence. After brutal losses in 2022, these positive factors drove the strong quarterly returns in Nasdaq. Comparatively, S&P 500 index returned 7.03%, while the DJ Industrial Average was little changed. European markets also staged a rebound, recouping a large part of the losses posted last year. In 2022, France’s Euronext Paris CAC 40 was down 9.50% and Germany’s FSE DAX fell 12.35%. In the first quarter, both of those beaten-down markets returned over 12%.

China: After the long-awaited reopening announcements from Chinese officials, the market started to trade higher on a release of the pent-up demand. China and Hong Kong also notched a gain like most markets, flipping from a whopping loss for two years. The markets entered the new year with a firm footing, but investors sought better visibility into the actual impacts.

The key benchmarks gave up a small amount of that return in the latter part of the quarter. Shanghai’s SSE Composite ended the three months up 5.94%, and Hong Kong’s Hang Seng Index returned 3.13%. Investors’ appetite for Chinese equities has improved. China Equity-A shares funds and China Equity funds attracted net flows of SGD 63.12 million and 48.67 million, respectively, for the quarter. Greater China Equity fuinds, which collected SGD 22.63 million, ranked eight. Other than China, equity funds investing in single Asian market or the Asia region were among the leaders in net flows. Net subscriptions of SGD 178.44 million to Asia-Pacific ex-Japan Equity funds led the board. Japan Flex-Cap Equity, Singapore Equity, Asian-Pacific Equity categories took the other spots in the top ten list.

Thematic Funds: Sentiment for thematic equity strategies was mixed. Investors favored tech equity funds but sold their units in healthcare, alternative energy, financial services, and natural resources sector funds.

Bond Investors Buy Global and U.S., Selling Asia

The banking crisis in the U.S. began to unfold as crypto-friendly bank Silvergate Capital said it would wind down its operations after the collapse of crypto exchange FTX.

Jerome Powell, chair of the U.S. Federal Reserve, told Congress that bringing down inflation “has a long way to go and is likely to be bumpy,” and the ultimate level of interest rates is likely to be higher than previously anticipated.

The next day, short-term yields peaked at 5.05%, marking the inversion between two- and 10-year Treasuries to its widest point since September 1981, to negative 107 basis points. A flight to quality dragged yields on two-year bonds to 4.06% at the end of March. Shorter- and longer-term bond yields are below the level of the end of 2022 but still above where they were a year ago.

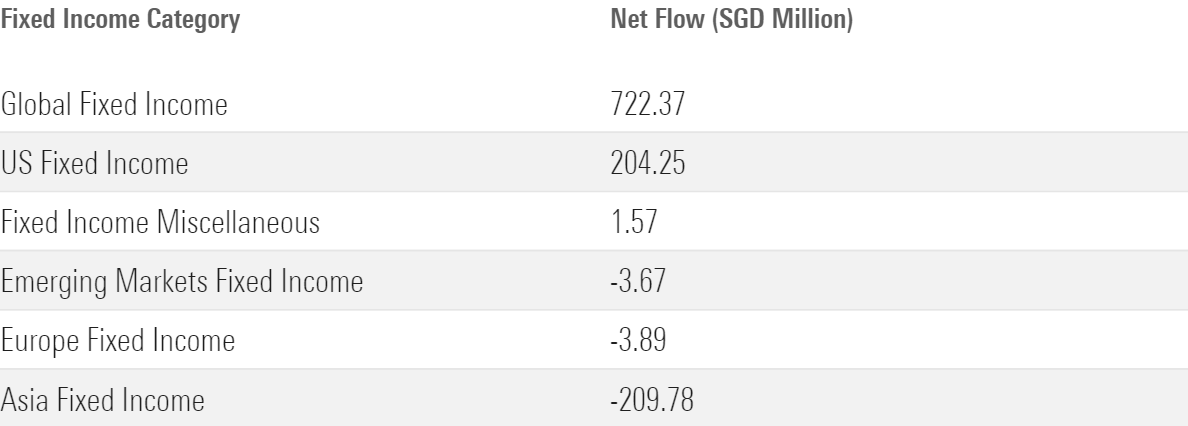

The FTSE WGBI rose 2.6% for the quarter (in U.S. dollars) versus a 2% loss from the fourth quarter. After the most recent hike of a quarter-percentage point, the target federal-funds rate reached 4.75%-5%, up from zero at the start of 2022. Global-bond MPFs returned 3.4%. Asian bond categories also generated around 3%, on average.

Against the backdrop, excluding global and U.S. fixed-income funds, all bond categories recorded outflows this quarter. Asia fixed-income funds continued to record the largest redemptions, as the category group ended the quarter with negative net flows of SGD 209.78 million, after the fourth quarter’s 327.98 million outflows. Emerging markets and Europe fixed-income funds posted small negative flows of around SGD 3 million.

The Outlook

Since the U.S. Federal Reserve began tightening monetary policy in 2022, the federal-funds rate has risen to a range of 4.75% to 5% from zero, the fastest and steepest tightening policy since the early 1980s.

Looking forward, if the U.S. economy weakens and inflation wanes, the Federal Reserve will have room to reverse course and begin to ease monetary policy at the end of this year.

At its March meeting, the Fed updated the language in its statement, removing “it anticipates ongoing increases”, replacing it with “anticipates that some additional monetary policy may be appropriate.” In addition, during the press conference, Chair Powell noted that the current issues among regional banks will result in tightening credit conditions that will have the same effect as one or more interest-rate hikes. At this point, it appears that we are either at, or near, the end of the current monetary tightening cycle.

Over the near term, investor sentiment could oscillate between positive news that hits the tape and unfavorable economic metrics releases. The market will need to see a turnaround in leading economic indicators to break through the top of this range and rally up toward where we see fair value. For investors with a long-term investment orientation, there is enough margin of safety in the market to use selloffs to judiciously add to equity exposures.

After lagging last year, stocks with a wide Morningstar Economic Moat Rating continue to be in favor and still have further to run. In addition to being able to generate excess returns on invested capital over the long term, wide-moat companies generally have greater pricing power. As such, they should be able to pass any cost increases on to clients and be able to better maintain their margins and thus their valuations in an inflationary environment.

If global growth slows, and it will likely manifest itself in weak demand for Asian goods and lower export figures to those selling to the U.S. and Europe. The full brunt of this slowdown has yet to come to fruition, and some disappointment could occur in the market. Industrials and some tech names, especially for companies whose orderbooks undershoot expectations, will be the first to feel the pain. For the rest of 2023, a mixed outlook for earnings will differentiate the markets, with China likely to outperform on this front as activity picks ups in the absence of pandemic lockdowns.

What Caused 2023's 'Everything' Rally?

What Caused 2023's 'Everything' Rally?

2023: Best and Worst Performing Stocks in Singapore

2023: Best and Worst Performing Stocks in Singapore

Upcoming changes to our membership offerings, tools, and features

Upcoming changes to our membership offerings, tools, and features

Highlights from the 2025 Morningstar Fund Awards (Singapore)

Highlights from the 2025 Morningstar Fund Awards (Singapore)

.png) 2025 Morningstar Fund Award Winners

2025 Morningstar Fund Award Winners

Asian High-Yield Bonds Rebound Strongly in 2024, but Caution Prevails for 2025

Asian High-Yield Bonds Rebound Strongly in 2024, but Caution Prevails for 2025

6 Undervalued US Stocks That Just Raised Dividends

6 Undervalued US Stocks That Just Raised Dividends

.jpg "Kate Lin")