Equities in emerging countries are slowing down after a good run over the last year. Traders and money manager are now starting to wonder if it still makes sense to focus on an asset that has always been considered useful in terms of diversification but which, even when things go well, carries abundant risks.

The Morningstar Emerging Markets Index in the last month (up to May 6) gained just 0.1 per cent, bringing the year-to-date performance to 4.9 per cent (18.4 per cent in 2020).

In four weeks, the Global Markets basket recorded 2.25 per cent (9.7 per cent since January; 16 per cent in 2020).

Morningstar Emerging Markets Index vs Morningstar Global Markets Index YTD

Source: Morningstar

“The road to successful investing in emerging markets is littered with holes and risks being expensive,” says Morningstar manager research analyst Daniel Sotiroff.

“The dangers facing investors in these countries are numerous and insidious. The problem is that traditional risk measures do not adequately capture elements ranging from bad corporate governance to political problems.”

Political risks

The political question, which is often linked to corruption phenomena, should not be underestimated. One of the most notable cases came to light in late 2015, when executives at Brazilian state oil company Petrobras became embroiled in an intricate web of bribes made up of company contractors, executives, and politicians. The scam drained the company's coffers while it lined the pockets of the parties involved.

"The harmful behavior of emerging-markets executives is nothing new," says Sotiroff. “We saw a lot of them in Russia in the late 1990s, when the country was trying to transition toward a capitalist democracy.”

More recently, in the late 2000s, it emerged that the (state-owned) natural gas giant Gazprom had sold off several major natural gas reserves to executives of the same company and some of their family members.

"These two cases show another distinguishing feature of emerging markets," says Sotiroff.

“Petrobras and Gazprom are companies that are partially or largely owned by their respective governments--a much more widespread phenomenon in emerging markets than in developed economies.

"State ownership increases the risk because the interests of politicians are not always in line with those of investors.

"Companies usually have the goal of maximising profits for shareholders, while the responsibilities of governments include the security of resources, foreign policy, and social welfare, to name a few. "

Fragile economies

Another risk of emerging areas is given by national economies that are usually more fragile in these areas than in developed areas such as the United States, Western Europe, and Japan. "This contributes to the volatility of their stock markets and can lead to the closure or even the collapse of entire financial markets," says Sotiroff.

According to the analyst, another element to consider is that the geographic composition of the baskets dedicated to emerging markets tends to change more frequently than that of the developed baskets. “And this leads to higher portfolio turnover,” he explains.

In the midst of all this, also consider the high costs of this type of investment that derive from having to do more research on shares that are often not very liquid. "There are also currency issues to consider. In the past we have also seen cases in which local turmoil has forced some emerging markets to close for long periods," says Sotiroff.

Better to leave emerging markets alone, then? “Overall, these risks don't paint a rosy picture, but that doesn't mean investors should avoid developing countries altogether,” the analyst says.

"On the contrary, dealing with greater dangers further underlines the importance of diversification when moving into these areas."

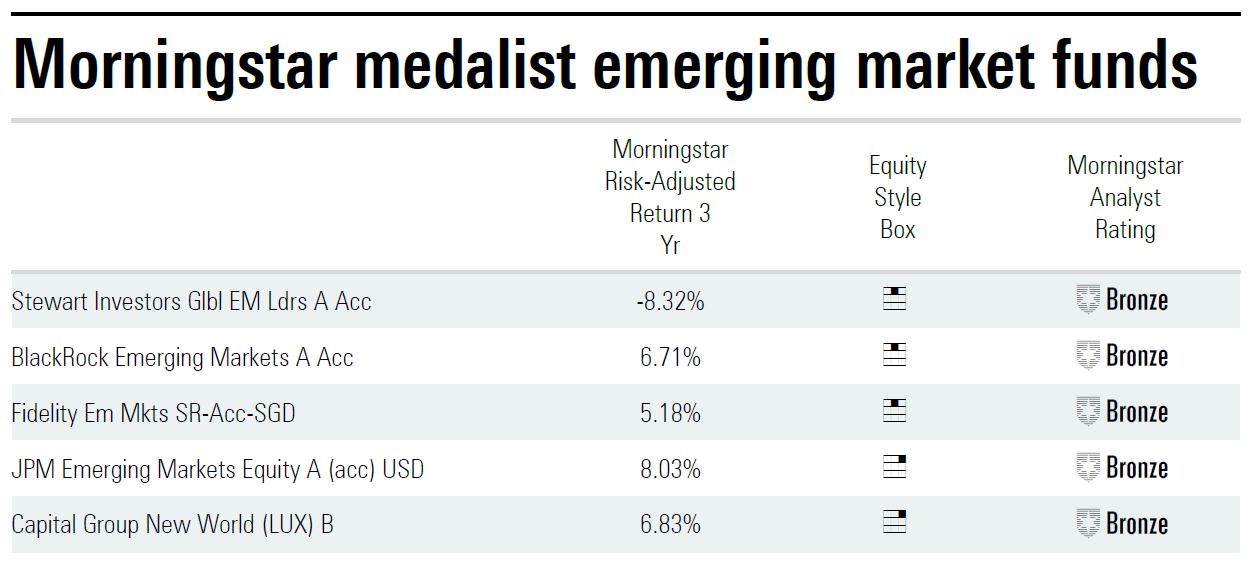

Source: Morningstar Direct, funds available for sale in Singapore.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)