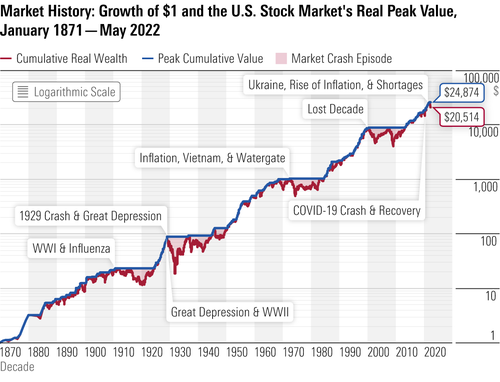

It’s usually fashionable to be late to a party, except of course when the stock market is throwing it.

In that case, the accepted wisdom is to arrive early before the good times get going. “Buying the dips” is standard stock market practice, referring to investors scooping up shares at perceived discounts during market swoons, in the expectation that they will resume their upward trajectories.

But bear markets are a different sort of animal than run-of-the-mill corrections. Rallies within a bear market can often be mistaken for the beginning of a new bull run, only to reverse course and head lower. Bottoms can be easily misjudged. Buying early in such cases often amplifies losses.

Should I Buy the Stock Dips?

While many bullish strategists say June 16 probably marked the lows in the stock market, bearish strategists are more skeptical. Last Monday’s steep selloff, the market’s worst one-day performance since June, highlighted the tug of war between the dueling views. It also showcased that buying the dips might not always make the best sense. That’s what the folks at Richard Bernstein Advisors, a New York City-based investment management firm with $14.3 billion under management, caution in a recent piece headlined ”Bubbles and Bears.”

“Many investors insist on buying early so that they can be there at the bottom,” says Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors. “In seven of the last 10 bear markets, it has been better to be late than early.”

Buying later rather than earlier, says Suzuki, more often than not improves returns, reduces downside potential, and provides more time to make informed decisions about the state of corporate profits and market liquidity to ensure some margin of safety.

Crunching the data around bear market bottoms based on hypothetical returns that included the six months before and the 12 months after the low, the firm’s analysis determined that portfolios that held 100% of their assets in cash (three-month Treasury bills) until six months after the bottom, before shifting 100% to stocks, outperformed those portfolios that were fully invested in stocks for the entire period.

Out with the Old and in With the New

Suzuki points out, too, that buying too early often leads to another common mistake that puts investors at a disadvantage: piling back into the leaders of the previous cycle. He advises paying attention to two trusted rules:

“Rather than rotating away from bubble assets, investors tend to view the initial price declines as attractive opportunities to buy secular growth at huge discounts,” says Suzuki. “Yet the history of bubbles suggests that they don’t return to being great investments after just six months of selling off.”

He points to the dot-com bust of 2000-02 that resulted in a bear market in the Nasdaq 100 Index that spanned 30 months, during which there were 16 bear market rallies that racked up gains of 10% to more than 30%. The index declined from March 2000 through October 2002 by 83%.

In the rally off the low of June 16 through Aug. 19, 2022, the Morningstar US Market Index gained 16.4% on a total return basis. For the year to date, the index is down 13.69%. After falling 32% through June 16, the Nasdaq 100 Index gained 19% from the low through Aug. 19. Through Aug. 25, the tech-heavy index is off 19% this year on a total-return basis.

Suzuki suspects when new areas of leadership emerge it will be strikingly opposite from the last time, which included U.S. large-cap growth, technology, and bonds. He is watching international stocks, small-cap stocks, and financials among other value-oriented investments.

“At this point in the cycle, it makes sense to focus on high-quality companies with stable cash flows and strong balance sheets, while avoiding bubble assets such as technology stocks and crypto,” Suzuki says.

Fed Still in Tightening Mode Argues Against Buying Dips

Suzuki notes that in the past 70 years there have been three bear markets in which investors benefited by buying stocks before a bottom: 1982, 1990, and 2020. The common denominator in those instances was that the Federal Reserve Board had already begun cutting interest rates. That’s not the backdrop against which this recent summer rally occurred. The Fed is still raising rates as it tries to meaningfully reduce still-high inflation.

After cratering Monday, the stock market teetered throughout the week ahead of the Federal Reserve’s annual summer confab at the Jackson Hole Economic Symposium. Stocks plunged again Friday after remarks by Fed chair Jerome Powell, in which he noted inflationary conditions warrant that monetary policy will likely remain “restrictive” for some time. Odds in the futures market increased for a September rate hike of 0.75% following Powell’s comments, according to the CME Group’s FedWatch Tool.

In a recent interview with The Wall Street Journal, Federal Reserve Bank of St. Louis president James Bullard said he “would lean toward the 0.75% at this point.”

“We’ve got relatively good reads on the economy, and we’ve got very high inflation, so I think it would make sense to continue to get the policy rate higher and into restrictive territory,” said Bullard.

The Fed will be making its decision as new evidence emerges that the economy is cooling, increasing worries that continued rate hikes may lead to a recession.

Earlier this week, the U.S. Census Bureau and the U.S. Department of Housing and Urban Development said new house sales in July fell to the lowest level since January 2016. New house sales have fallen six out of seven months this year.

In addition, S&P Global's August flash indexes of purchasing managers surveyed in the manufacturing and nonmanufacturing arenas showed sharp drops in business activity. Sian Jones, senior economist at S&P Global Market Intelligence, noted the fall in total output “was the steepest seen since the series began nearly 13 years ago,” excluding the period between March and May 2020.

“Given the high likelihood that the Fed will continue to tighten into already slowing earnings growth, it seems premature to be significantly increasing equity exposure today,” says Suzuki.

.png)